ЛНР, Российская Федерация, Луганск

СДЕЛАЙТЕ СВОИ УРОКИ ЕЩЁ ЭФФЕКТИВНЕЕ, А ЖИЗНЬ СВОБОДНЕЕ

Благодаря готовым учебным материалам для работы в классе и дистанционно

Скидки до 50 % на комплекты

только до

Готовые ключевые этапы урока всегда будут у вас под рукой

Организационный момент

Проверка знаний

Объяснение материала

Закрепление изученного

Итоги урока

Была в сети 16.02.2026 15:43

Недодаева Анастасия Владимировна

Преподаватель английского языка

40 лет

Местоположение

Специализация

320 группа Задание 07.03.2025

Категория:

Английский язык

10.03.2025 12:53

Просмотр содержимого документа

«320 группа Задание 07.03.2025»

Saturday, the 7th of March

Classwork

Read and translate the text and put the table in the copybook. Прочитать и перевести текст о банках и начертить таблицу в тетради.

Составить 10 вопросов к тексту.

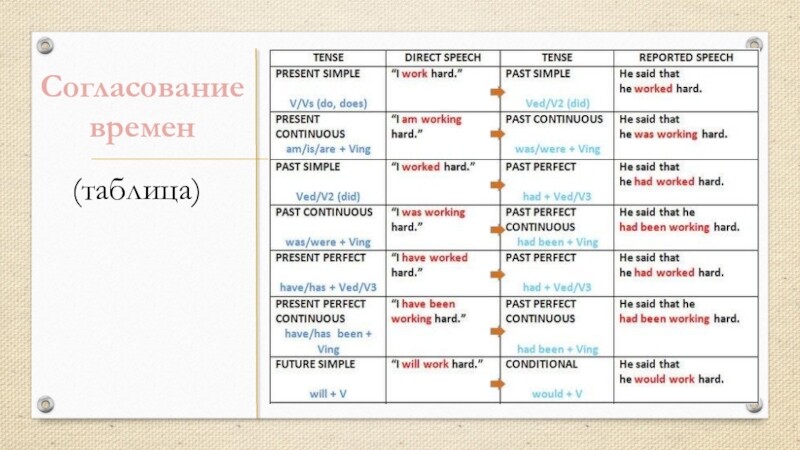

Пересказать текст, используя правило согласования времен. Выучить правило.

If you're looking to open a business bank account, a personal account, or looking for a loan or investments, it's essential to know about the different types of banks you can do business with.

This is because different banks and other financial institutions operate differently, offering different services and providing different benefits. Therefore, it's essential to conduct thorough research before choosing which bank to partner with or use.

In this article, we will discuss the different types of banks and their key features and provide some insight into which type of bank is most suitable for you.

What is a Bank, and How Does It Operate?

Before exploring the different types of banks, it's essential to understand the basic concept of a bank.

Banks are financial institutions authorized to accept deposits and provide credits. Along with fundamental functions, they offer an array of services, including:

Credit cards.

Check-cashing services.

Wealth management services.

Insurance.

Business banking.

The core operation of banks involves using customer deposits as a base for lending. Banks lend these funds to other customers at a higher interest rate than they pay on deposits. This interest rate spread is a primary source of their profit.

Additionally, banks generate revenue through service fees and charges, including account maintenance, transaction fees, and specific service charges like overdrafts and wire transfers.

This operational model positions banks as vital intermediaries between savers and borrowers. They facilitate the circulation of money within the economy, contributing significantly to both financial growth and stability.

How Are Banks Regulated?

Banks are regulated by government bodies and the central bank to ensure safety, ethical operations, and financial stability. These regulations include capital adequacy and liquidity requirements, ensuring banks maintain sufficient reserves and liquid assets. In addition, risk management protocols are also mandated, along with regular audits, to guarantee compliance.

Consumer protection laws play an integral role in banking regulation. These laws are designed to safeguard customers from unfair banking practices and ensure transparency. Moreover, banks often participate in government-backed insurance schemes, such as the FDIC in the U.S. This scheme covers deposits up to USD250,000 per depositor per bank to protect depositors in case of bank failures. These regulations ensure that banks operate responsibly and in the public and economic interest.

| Types of Banks | What It Is | Key Services | Suitable for |

| Retail Banks | Banks that offer services to individuals | Bank accounts, loans, debit and credit cards, and ATMs. | Individuals and small businesses |

| Commercial Banks | Banks designed for commercial purposes | Loans, cash management, credit products, equipment lending, trade finance, commercial real estate, foreign exchange | Small and mid-size businesses |

| Investment Banks | Banks that manage investment portfolios | Stock trade, securities, and bonds management, corporate finance, merger & acquisition assistance, and asset management | Large corporations, and institutional investors |

| Universal Banks | Banks that offer a combination of retail, commercial, and investment banking services–all in one place | Checking and Savings Accounts, Credit and Loan Facilities, Brokerage Services Asset, Management and Investment Advisory, and Financial Analysis | Individuals and businesses seeking comprehensive financial services from one single bank |

| Credit Unions | Member-owned and non-profit financial institutions | Similar services to retail and commercial banks, but only to certain demographics | Individuals seeking affordability and local support |

| Private Banks | Banks offering personalized banking services | Financial planning, investment guidance, wealth management, credit services, lending | High-net-worth individuals |

| Savings and Loan Associations (S&Ls) | Banks specializing in making mortgage loans | Mortgages, refinance loans, and alternative home loans using deposited savings | Customers seeking a community-oriented banking experience for homebuying |

| Islamic Banks | Banks that operate in strict adherence to Islamic law. | Profit and Loss Sharing Ventures, Cost Plus Finance, Islamic Leasing, Islamic Bonds, and Islamic Insurance | Individuals and businesses seeking financial institutions that comply with Islamic law |

| Green Banks | Banks that focus on funding renewable energy, energy efficiency, and other green initiatives, rather than maximizing profits. | Financing Renewable Energy Projects, Energy Efficiency Financing, Funding for Low-Carbon Technologies, Climate Resilience and Adaptation Projects, Mobilizing Private Investment, and Advisory Services | People and organizations need financial support to transition or create eco-conscious projects and technologies. |

| Challenger banks | New banks that challenge traditional banking models by offering innovative products and services | Savings accounts, investment accounts, mobile banking | Individuals and businesses seeking convenience and remote banking |

| Neobanks | Digital-only banks that operate entirely online with no physical branches | Multi-currency accounts, mobile banking | Individuals and businesses seeking innovative 100% banking options |

Комплекты видеоуроков для учителей

Скачать

© 2025, Недодаева Анастасия Владимировна 125 0

Похожие файлы

Вебинар для учителей

Свидетельство об участии БЕСПЛАТНО!