Россия, Нижний Новгород

СДЕЛАЙТЕ СВОИ УРОКИ ЕЩЁ ЭФФЕКТИВНЕЕ, А ЖИЗНЬ СВОБОДНЕЕ

Благодаря готовым учебным материалам для работы в классе и дистанционно

Скидки до 50 % на комплекты

только до

Готовые ключевые этапы урока всегда будут у вас под рукой

Организационный момент

Проверка знаний

Объяснение материала

Закрепление изученного

Итоги урока

Была в сети 16.08.2022 14:41

Кузнецова Светлана Ивановна

Преподаватель английского языка

61 год

Местоположение

Специализация

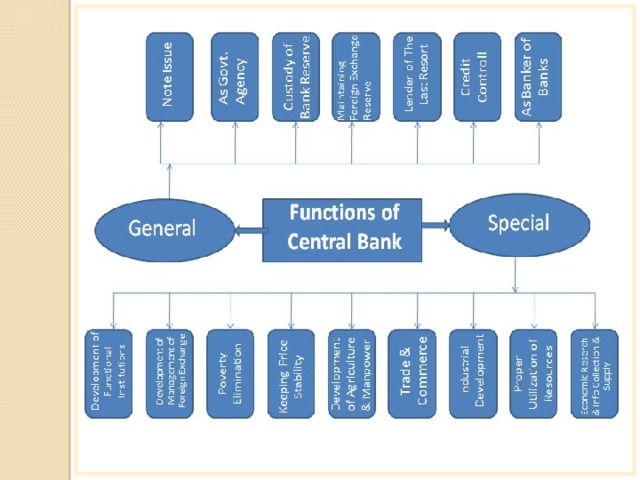

The Functions of Banks

Категория:

Английский язык

23.02.2019 22:08

Просмотр содержимого документа

«The Functions of Banks»

The Functions of Banks

Презентация выполнена преподавателем английского языка

«Нижегородского Губернского колледжа»

Кузнецовой Светланой Ивановной.

A Bank is a financial institution which is involved in borrowing and lending money.

Banks take customer deposits in return for paying customers an annual interest payment.

The bank then use the majority of these deposits to lend to other customers for a variety of loans.

REMEMBER!

Main purpose of banks:

- Keep money safe for customers.

- Offer customers interest on deposits, helping to protect against money losing value against inflation.

- Lending money to firms, customers and homebuyers.

- Offering financial advice and related financial services, such as insurance

The most important functions

of commercial banks

1) Accepting Deposits from the public :

Various sections of society, according to their needs and economic condition, deposit their savings with the banks.

- Fixed and low income group people deposit their savings in small amounts from the points of view of security, income and saving promotion.

- Traders and businessmen deposit their savings in the banks for the convenience of payment.

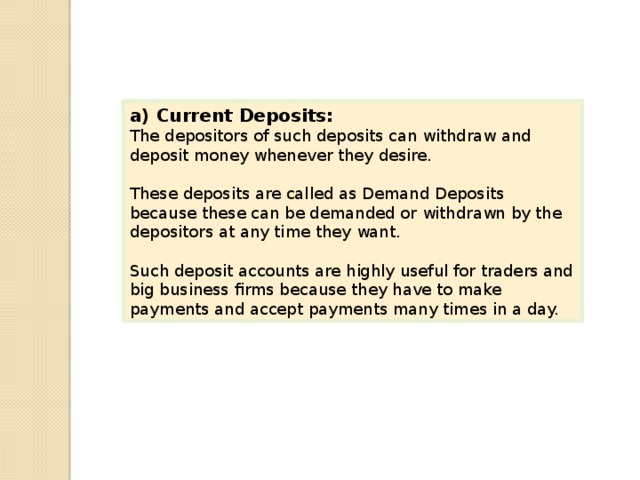

a) Current Deposits:

The depositors of such deposits can withdraw and deposit money whenever they desire.

These deposits are called as Demand Deposits because these can be demanded or withdrawn by the depositors at any time they want.

Such deposit accounts are highly useful for traders and big business firms because they have to make payments and accept payments many times in a day.

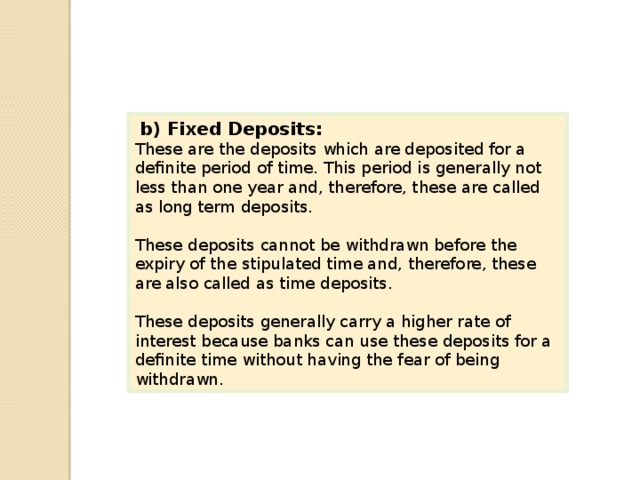

b) Fixed Deposits:

These are the deposits which are deposited for a definite period of time. This period is generally not less than one year and, therefore, these are called as long term deposits.

These deposits cannot be withdrawn before the expiry of the stipulated time and, therefore, these are also called as time deposits.

These deposits generally carry a higher rate of interest because banks can use these deposits for a definite time without having the fear of being withdrawn.

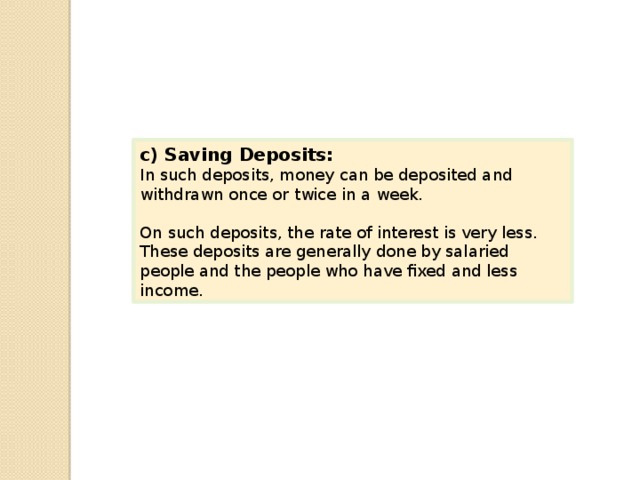

c) Saving Deposits:

In such deposits, money can be deposited and withdrawn once or twice in a week.

On such deposits, the rate of interest is very less. These deposits are generally done by salaried people and the people who have fixed and less income.

2) Giving Loans:

The second important function of commercial banks is to advance loans to its customers. Banks charge interest from the borrowers and this is the main source of their income.

Banks advance loans not only on the basis of the deposits of the public rather they also advance loans on the basis of depositing the money in the accounts of borrowers. In other words, they create loans out of deposits and deposits out of loans. This is called as credit creation by commercial banks.

3) Cash Credit:

Banks advance loans to its customers on the basis of bonds, inventories and other approved securities. Banks enter into an agreement with its customers to which money can be withdrawn many times during a year.

Under this set up banks open accounts of their customers and deposit the loan money. With this type of loan, credit is created.

4) Demand loans:

These are such loans that can be recalled on demand by the banks. The entire loan amount is paid in lump sum by crediting it to the loan account of the borrower, and thus entire loan becomes chargeable to interest with immediate effect.

5) Short-term loan:

These loans may be given as personal loans, loans to finance working capital or as priority sector advances.

These are made against some security and entire loan amount is transferred to the loan account of the borrower.

6) Over-Draft:

Banks advance loans to its customer’s upto a certain amount through over-drafts, if there are no deposits in the current account.

For this banks demand a security from the customers and charge very high rate of interest.

7) Discounting of Bills of Exchange:

This is the most prevalent and important method of advancing loans to the traders for short-term purposes.

Under this system, banks advance loans to the traders and business firms by discounting their bills. In this way, businessmen get loans on the basis of their bills of exchange before the time of their maturity.

8) Investment of Funds:

The banks invest their surplus funds in three types of securities—

- Government securities,

- approved securities.

- other securities.

Government securities include both, central and state governments, such as treasury bills, national savings certificate etc.

Other securities include securities of state associated bodies like electricity boards, housing boards .

9) Agency Functions:

Banks function in the form of agents and representatives of their customers. Customers give their consent for performing such functions. The important functions of these types are as follows:

- Banks collect cheques,drafts, bills of exchange and dividends of the shares for their customers.

- Banks make payment for their clients and at times accept the bills of exchange: of their customers for which payment is made at the fixed time.

- Banks pay insurance premium of their customers. Besides this, they also deposit loan installments, income-tax, interest etc. as per directions.

- Banks purchase and sell securities, shares and debentures on behalf of their customers.

- Banks arrange to send money from one place to another for the convenience of their customers.

10) Miscellaneous Functions:

- Banks make arrangement of lockers for the safe custody of valuable assets of their customers such as gold, silver, legal documents etc.

- Banks give reference for their customers.

- Banks collect necessary and useful statistics relating to trade and industry.

- For facilitating foreign trade, banks undertake to sell and purchase foreign exchange.

- Banks advise their clients relating to investment decisions as specialist

- Bank does the under-writing of shares and debentures also.

- Banks issue letters of credit.

- During natural calamities, banks are highly useful in mobilizing funds and donations.

Вебинар для учителей

Свидетельство об участии БЕСПЛАТНО!